How Much Mortgage Can I Afford?

Many people wonder, “How much mortgage can I afford?” Homeownership isn’t easy, especially with the rising costs of debt and consumer goods. The loan payment is just one part of the expense, and you’ll also have to pay for homeowner’s insurance and taxes. If you can’t afford to make all of these monthly payments, you may want to consider buying a smaller home or renting. Here are some tips to help you find the right mortgage for you.

Calculating your monthly mortgage payment

One of the biggest investments you will make is buying a home. The purchase price of your home is likely to be your largest, and you will need to take out a mortgage to finance the purchase. However, the mortgage payment is not the same as the loan amount divided by the number of months. This article will explain how to calculate your monthly mortgage payment, and how to avoid surprises that may occur. It also shows you how to use an online mortgage calculator to figure out how much your payment should be.

There are many different ways to calculate your mortgage payment. Using a mortgage calculator can help you determine your monthly payment, interest rate, and loan terms. Once you have a basic idea of what you can afford, you can start adjusting variables in the mortgage calculator. This will give you a more accurate idea of how much you can afford to borrow. This will ensure that you do not overextend yourself and end up “house poor.”

Getting pre-approved for a mortgage

Before searching for a home, getting pre-approved for a mortgage is an important first step. This letter shows the lender that you’re approved to receive a certain amount of money for your mortgage. Generally, a pre-approval letter will say how much money you can spend on the home and what interest rate you can expect. While getting pre-approved does not guarantee you’ll get the home of your dreams, it can help you find a home faster.

Getting pre-approved can be intimidating, but it can help you understand your finances better. It forces you to examine your current financial status and get it on track. Lenders can also help you remedy any issues with your credit before your application is reviewed. It also allows you to get an idea of the cost of homeowner’s insurance, real estate taxes, and other miscellaneous expenses. A pre-approval can help you avoid those surprises by minimizing the risk of a loan approval denial.

Calculating your debt-to-income ratio

Your debt-to-income ratio (DTI) is a simple calculation that measures how much you can afford to spend on big purchases. Usually, you can lower your DTI by paying off your debts, increasing your income, and avoiding taking on more debt. To calculate your DTI, add up all of your monthly minimum payments and divide them by your gross monthly income. You will get a percentage of your debts.

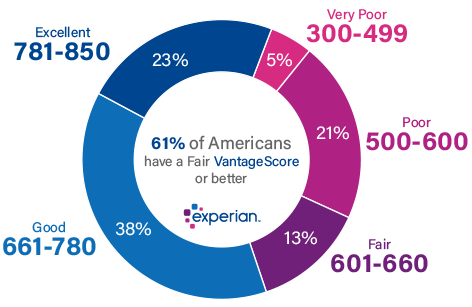

When applying for a mortgage, your debt-to-income ratio is one of the most important factors lenders consider. It informs lenders if you can pay off your loan or incur more debt. The lower your ratio is, the better. A high number, on the other hand, means you are a risk for the lender. To help you understand whether your debt-to-income ratio is too high, consider determining your debt to income ratio by reviewing your income and expenses.

Buying a smaller home

How much mortgage can I afford when buying a smaller home? You must first create a budget and then determine when to buy. If you can’t afford to buy now, you can wait a year or two and focus on saving up a down payment and improving your credit score. The better your financial situation is, the more money you can afford to spend on a mortgage. The guidelines for determining mortgage qualification are listed below.

You should look for a home priced at three to five times your annual income. If you have no debt and a stable job, you can look at the upper end of the range. If you have significant debt, it’s better to look at a lower priced home. You should work with a real estate agent to help you set realistic expectations. The agent may be aware of home sales that other people might not know about.