Whether you’re buying a home or selling one, it’s always good to have an idea of what title insurance doesn’t cover. After all, how can you be sure that you’re not making any unnecessary mistakes?

Abstract

Whether you’re a first time homebuyer or a seasoned pro, knowing your home has an unbroken chain of title is a good thing. Similarly, knowing that your lender has a solid title insurance policy is an added benefit. In other words, be on the lookout for any unforeseen pitfalls.

The best way to ensure you’re on the right track is to scout out your property and take the time to familiarize yourself with its history. A quick perusal of the property’s record books is a good start. Be on the lookout for any encroachments that may have gone unnoticed by your real estate agent. Similarly, be sure to read the title deed before you ratify the contract.

The best way to determine which of the many title insurers is best for you is to shop around. Getting the best rate will pay dividends in the long run.

Cloud on title

Usually, when a buyer buys a property, they do a title search to find out if there are any title issues. If there are any, they may need to clear the cloud on title before the sale can be completed. This could add time and money to the process, making it more difficult for the seller to complete the sale.

There are different types of defects that could cloud the title. The most common is a mortgage lien. If the mortgage is unpaid, the lender will put a lien on the property. The lien tells potential buyers that the homeowner is behind on their payments. Fortunately, a mortgage lien can be lifted once the seller has paid off the loan.

Another type of defect is an undisclosed easement. An easement gives a utility company the right to access certain parts of the property. If the easement is not disclosed, it can cause a title issue.

Complaint handling protocol

Having a top notch customer service rep is not a bad idea, but a bit of TLC goes a long way. The best way to avert a dispute is to make your clients happy before they become a customer. Providing the top of the line customer service is not only rewarding, it also helps you retain your squeaky clean clientele. To keep your clientele in line, it’s a good idea to implement a complaint handling protocol that consists of two parts – a top notch customer service department and a customer-centric employee training program. This will ensure a smooth, stress-free, and pliable customer experience. To avert a potential catastrophe, it is imperative that you adopt a customer-centric approach to all business decisions. This will not only lead to a healthier clientele, it will also lead to higher employee morale and greater productivity.

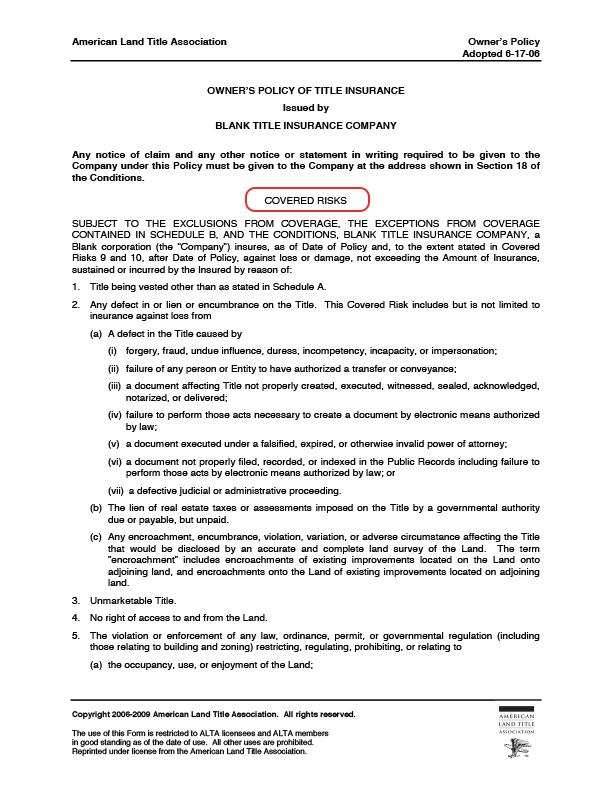

Owner’s policy

Whether you are a first time buyer or a long time home owner, you might want to consider purchasing an Owner’s policy. This is a type of insurance that protects you against claims or losses due to problems with the title of your property.

This insurance is important because it can save you money. In addition to protecting you against title problems, it can also cover costs incurred due to litigation. The cost to defend yourself in a lawsuit can be huge.

It is not a legal requirement for all buyers, but you might want to get an owner’s policy anyway. An owner’s policy can help you sell your home more quickly, and it may even provide you with a cash settlement if you are the victim of a lien.

Lender’s policy

Generally, there are two types of title insurance policies: lender’s and owner’s. The difference is in the extent of coverage. Lender’s insurance only covers the amount of the loan or the outstanding secured debt, while an owner’s policy protects the value of the property at the time of a claim.

Lender’s insurance is required by most mortgage lenders. The cost of this type of insurance is usually lower than an owner’s policy. It’s also necessary for borrowers to purchase this type of insurance. It’s a small expense.

Lender’s insurance policy protects the mortgage lender’s interest in the property. It also ensures the first lien in the event of a foreclosure or an unpaid property tax. This is because the policy is based on the amount of the loan. In addition, the lender’s policy includes the original named lender, its successors, and its assigns.